Market Outlook (GBP, EUR & USD) April 2025

Share

GBP

The pound was on track for a second straight monthly advance in March, rallying around 3% against the dollar, with cable briefly trading north of the $1.30 mark, to its best levels since last autumn.

These gains, however, came largely by virtue of a broadly weaker USD, as opposed to any GBP-specific catalysts. This helps to explain the monthly decline notched by GBP/EUR, with the cross backing away from the 1.20 handle as March progressed.

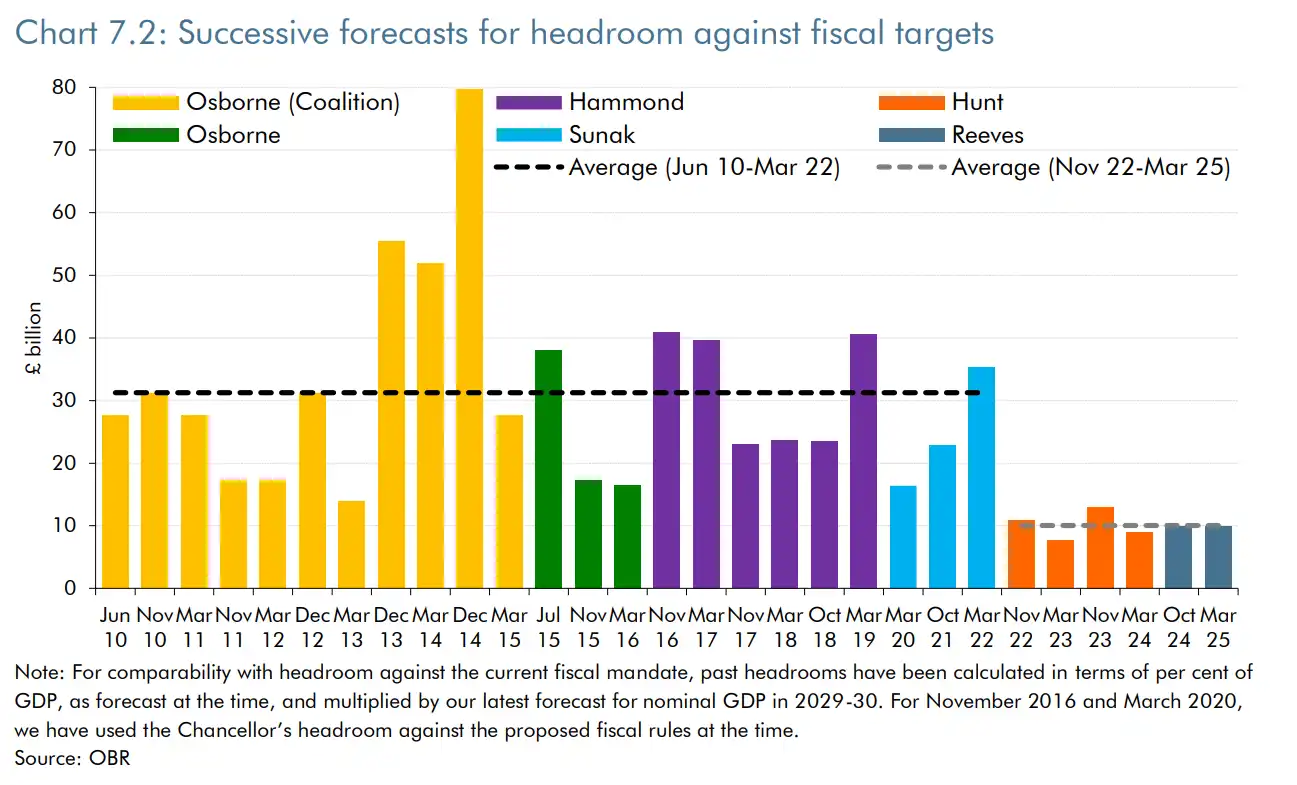

Focus during the month fell largely on the UK’s fiscal backdrop, with Chancellor Reeves delivering the Spring Statement towards the end of March. Given the anaemic economic growth, and sharp rise in Gilt yields, seen since the autumn Budget, said statement saw around £15bln of spending cuts delivered in order to ʻbalance the books’, and restore fiscal headroom to the £9.9bln level at which it stood six months ago.

Such a margin, though, is less than a third of the pre-covid average headroom that the Treasury typically operated with, in turn leaving the UK extremely exposed to any minor negative economic shocks. Were such a shock to eventuate, or the economy to evolve in a bleaker fashion than the OBR’s forecasts, further fiscal tightening would be required, as the aforementioned headroom would be eroded once more.

Hence, it seems inevitable at this stage that the Budget in six months’ time will bring about further spending cuts, and likely significant tax hikes too, both policies which will pose significant headwinds to the UK’s already-dismal economic growth outlook.

That outlook, of course, is not only one of sluggish economic growth, but also of stubbornly high inflation.

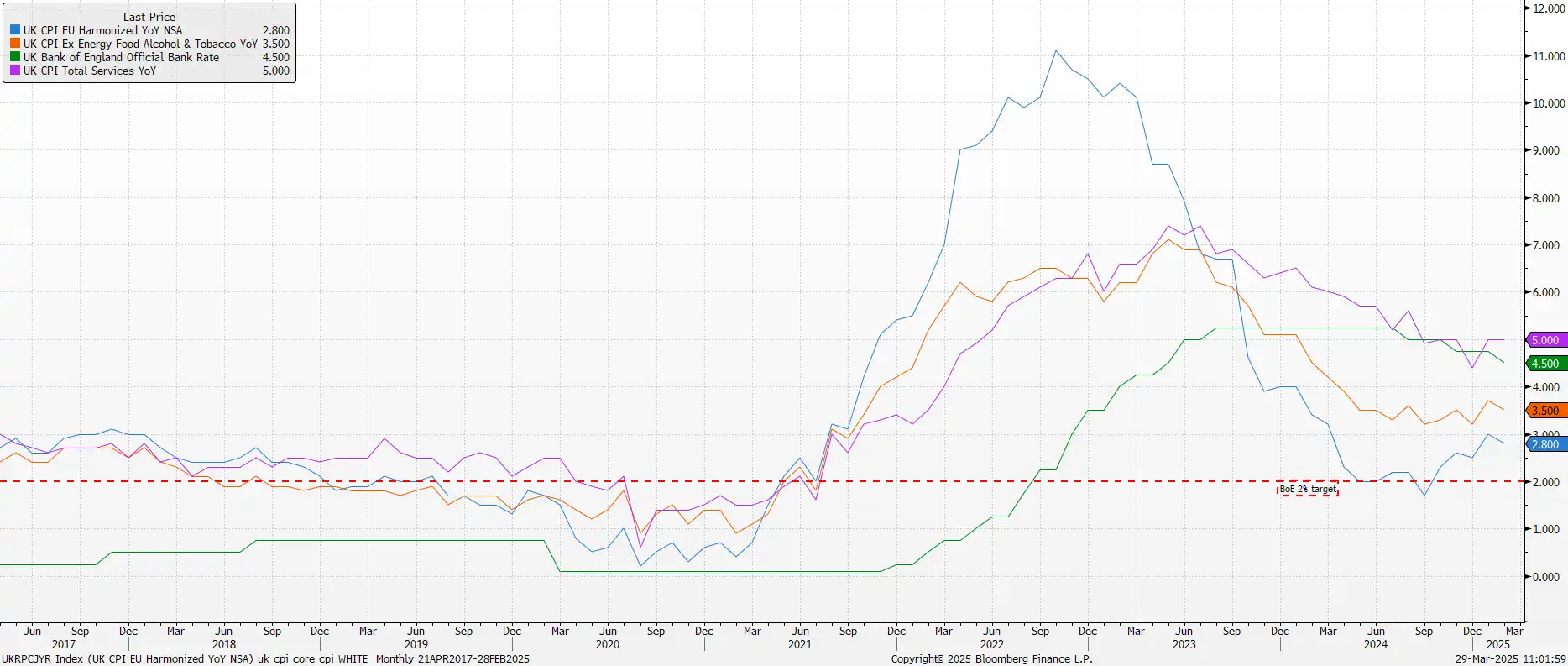

Though February’s inflation figures were cooler than market participants, and Bank of England policymakers had been expecting, it remains far too early to sound the ʻall clear’ just yet. Headline CPI rose 2.8% YoY in the second month of the year, though price pressures remain on course to intensify further over the coming months, as businesses pass through the impact of April’s National Insurance hike in the form of higher prices, and as further increases in energy prices push headline inflation towards 4% by the end of summer.

Against such a backdrop, it was no surprise to see the Bank of England hold Bank Rate steady at 4.50% at the conclusion of the March MPC meeting, with just one policymaker – external member Dhingra – dissenting in favour of a 25bp cut.

The direction of travel for Bank Rate, however, remains lower, albeit in “gradual and careful” fashion, as the MPC like to remind at every possible opportunity. The base case remains that 25bp cuts will be delivered once per quarter, likely in line with the release of updated economic forecasts, as part of the Monetary Policy Report.

Risks around that view, though, have become a touch more two-sided of late, particularly with services inflation remaining stubbornly above 5.0% YoY, increasingly provoking concern over the stickiness of underlying price pressures within the UK economy.

Said stickiness will, clearly, not be helped by the potential imposition of US tariffs at the start of April, with headlines on the trade front likely to be the market’s main focus in the short-term. While the UK’s goods exports are, these days, minimal in the grand scheme of things, a tit-for-tat transatlantic trade war, and the uncertainty that such a conflict would provoke, will likely act as a further significant economic headwind for businesses and consumers alike to battle against.

EUR

The common currency is on track for a near-5% gain in March, vaulting higher against most major peers, and with EUR/USD on track for its best monthly advance since November 2022.

This sizeable rally has taken the common currency from the cusp of parity earlier in the year, towards a test of the 1.10 figure in mid-March, though a break above that key psychological resistance has been a bridge too far for the time being.

These chunky gains for the EUR came amid a dramatic shift in the macroeconomic backdrop, upending years of fiscal conservatism in the bloc’s largest economy.

As expected, CDU/CSU candidate Merz emerged as the victor in Germany’s federal elections, and is on course to become the new Chancellor, in a coalition government with the SPD. However, even before taking office, Merz has taken decisive action, unveiling a 500bln EUR defence and infrastructure fund, finally turning on the fiscal spending taps, and delivering a much-needed fillip to the stalling German economy.

In turn, participants have re-assessed what was previously an incredibly pessimistic view not only of Germany’s economic prospects, but also of Europe’s place in the global geopolitical order, which had come under threat as a result of President Trump’s ʻAmerica First’ stance.

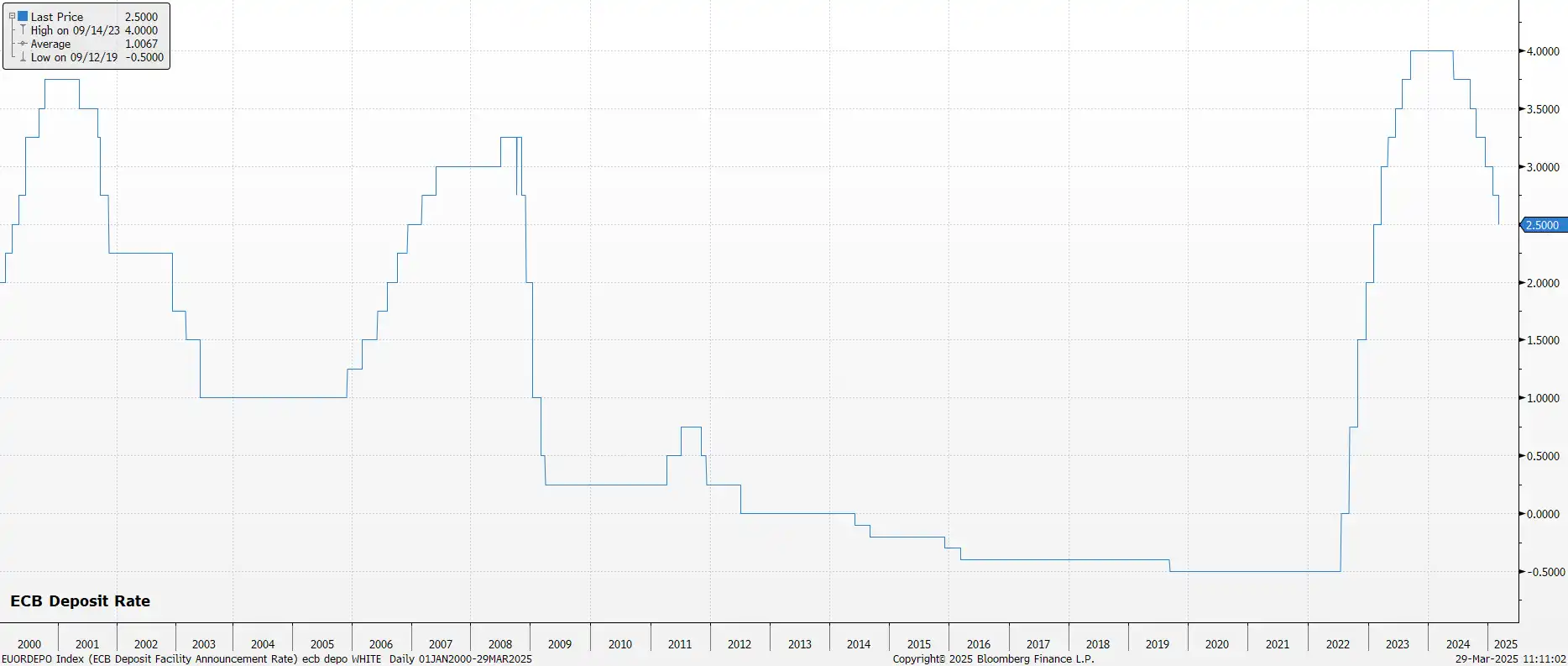

Nevertheless, 500bln EUR of spending will not solve all of the bloc’s issues in one fell swoop, with the multiplier effects of the fiscal package only becoming clear in the fullness of time. As a result, and with inflationary pressures of relatively little concern within the bloc, the ECB delivered another 25bp rate cut last month, lowering the deposit rate to 2.50%.

That rate cut, however, was accompanied by a significant tweak to the Governing Council’s policy guidance, with policymakers noting that rates are “becoming meaningfully less restrictive”, a nod to both the deposit rate having now reached the top end of neutral rate estimates, and to a potentially slower pace of policy easing moving forwards.

As a result, the April meeting is likely to see the Governing Council considerably more divided on the appropriate course for policy than at any point during this cycle. Even if a 25bp cut weren’t to be delivered, though, further rate reductions are near-certain at this moment in time, especially with headline inflation remaining on course to achieve the 2% target later this year.

The ECB will also be seeking to, as much as possible, cushion the eurozone economy from the impacts of President Trump’s protectionist trade policies.

The recent announcement of a 25% tariff on automobile imports to the US poses another substantial downside risk to the bloc’s beleaguered manufacturing sector, with broader downside growth risks also remaining significant, amid the likelihood of the US imposing reciprocal tariffs at the start of April.

USD

The greenback endured a difficult March, with the dollar index (DXY) on track to notch a third straight monthly decline for the first time since mid-2024, primarily as participants unwound ʻTrump Trades’ en masse.

This unwinding came as participants begun to adjust their expectations for the economic effects of the Trump Administration’s policies, and increasingly became concerned over the downside risks that the imposition of tariffs, along with efforts to slash the size of the federal government, would have on the US economy.

Perhaps the biggest concern, however, is the incoherence with which policy continues to be made, and the uncertainty that this subsequently causes. A prime example of this was seen towards the middle of March, where US trade policy towards Canada changed six times in the space of seven days, including twice in a 12 hour spell! Clearly, this ʻtariff by social media’ approach is making it impossible for any business, or consumer, to plan for the future, while also making it incredibly difficult for market participants to accurately price risk.

Furthermore, short of being the safe haven that participants would typically flock to in times of uncertainty, like the present, the dollar is actually finding itself bearing the brunt of the market’s ire, with the idea of ʻUS exceptionalism’ now stone dead, and with the greenback being the most exposed of all major currencies to the whims of President Trump.

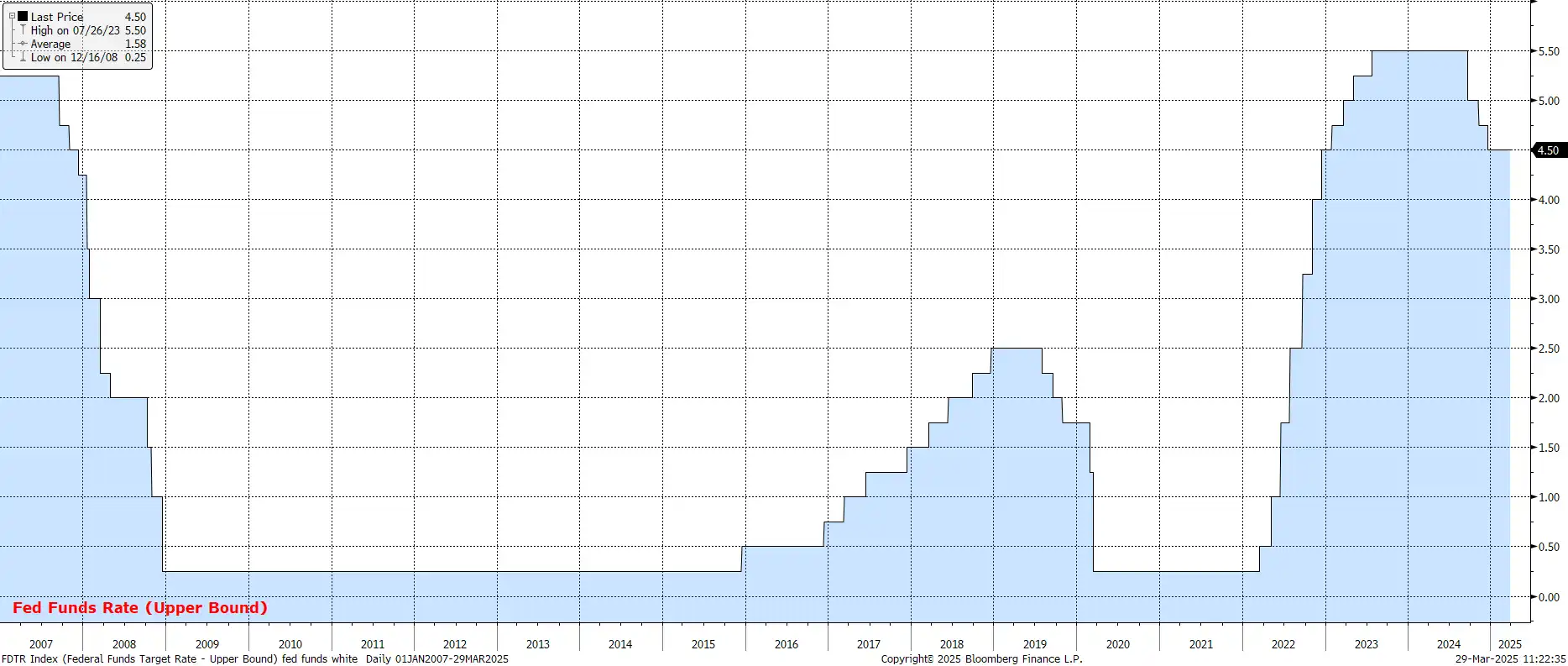

In any case, against this incredible degree of uncertainty, it came as no surprise that the FOMC maintained the target range for the fed funds rate at 4.25% to 4.50% at the conclusion of the March meeting.

Clearly, and understandably, policymakers remain firmly in ʻwait and see’ mode for the time being, having also maintained their projections for two 25bp cuts to be delivered this year, even as growth forecasts were cut, and the inflation profile raised. That said, the FOMC continue to project growth around 2% YoY, far quicker than the ʻstagflation’ scenario that some appear to increasingly be pointing towards.

The FOMC did, however, tweak the process of balance sheet run-off, or QT, cutting the monthly Treasury redemption cap to $5bln, from $25bln. Such a sluggish pace means, for all intents and purposes, QT is now at an end, which should provide a boost for Treasuries at the long-end of the curve. This, though, will likely prove a headwind for the dollar, as US-RoW spreads continue to narrow, a move which has already come a long way, as investors brace for a deluge of Bund issuance.

Fundamentally, though, the month ahead will again be all about tariffs, particularly with the announcement of reciprocal levies due on 2nd April, ʻLiberation Day’. Participants will also, though, be paying close attention as to whether recent softness in sentiment surveys begins to feed into ʻhard’ data, with signs of cracks appearing in either the labour market, or consumer spending, unlikely to be looked upon favourably, given mounting downside growth risks.